The Real Estate Guys recently invited our very own Steve Olson to host a webinar to answer live questions about FIG, our process, and much more (some of these questions shown below)

A Few of the Questions Asked/Answered:

- “How long from the start of conversation until the close of escrow?”

- “Do owners have to use FIG property management?”

- “Is FIG’s management always on-site full-time?”

- “Do you build on individual lots?”

- “Your pro forma refers to maintenance and repairs as “cleaning and maintenance.” It seems too low. Not sure what it’s designed to cover, but in my opinion, it would never cover replacing a roof, HVAC, water heaters, etc. over time…”

- “Do you always build communities with an HOA?”

Transcription of the Video:

We love working with the Real Estate Guys and we’ve been talking with them a lot lately about what it is we’re doing over here and they felt like we should go a little bit deeper and give those who want to, the chance to look a little bit more into what it is that we’re doing.

It’s kind of intended to be a Q&A type of session. We’re going to get into a little bit about what FIG is the Fourplex Investment Group, the process of what it’s like to invest in one of these fourplexes. We’re also going to get into where we do this, what some of the current opportunities look like, and some of the cool tax advantages that come from new construction fourplex investing.

My name is Steve Olson with the Fourplex Investment Group. We like to say that fourplexes are interesting, because if you were to look at the coin of real estate investing, and I’m speaking residentially, on one side, you’ve got single family on one side, you got multifamily. Fourplexes are actually just on the border there. They’re on the edge, and you get some good advantages from both sides of that coin.

Many of you had the chance to send in questions ahead of time. And I’ve listed a few of those here. And we’ll of course, like I said, depending on our timing, I’m trying to get you out of here in an hour. We may take some more, but I’ll give you my contact info. So you can ask any questions that you want to. But I’m going to read some of these questions because I want you to listen, throughout the presentation, these are going to get answered. And we’ll dig deeper knowing that you’ve asked these but Jill wanted to know how long from the start of construction until the close of escrow. Right, we’ll definitely cover that.

Andrew had a few questions you know about amenities? Do we have to use your property management? Are they on-site? What about just like one-off builds? Are these always in big masterplan communities with the HOA, and I apologize. Unknown, I had written this down and kind of messed up, I ended up having fat fingers on my keyboard, and I deleted the name of the individual asking if you know who you are probably. But talking about, hey, the cleaning and the maintenance on your performance looks really low. What’s up with that? So that’s a good question. We’ll definitely cover that.

Many of these are addressed on our website, if you get a chance to feel free to go to www.fig.us/faq. That’s where we’ve got a lot of the frequently asked questions that investors who are really putting their brains on this topic tend to think about, so a lot of those are covered there.

So that being said, the age of the attorney, right, I’ve got this disclaimer slide. I’m not going to read it to you verbatim, but it essentially says that your big boys and girls, we’re going to talk about investments here, verify this stuff, right? Don’t just take my word for it, please go out and independently verify it and make sure that you’re okay with it for your own investment purposes. Okay, so, let’s get started.

Let’s talk about how this really came to be. To my knowledge. FIG is the only company in the country that really builds fourplexes in mass. I know that there are one or two builders in Texas that do this here and there, and I’ve heard of a few others popping up but nobody has the footprint that FIG does. The reason being is that we thought it was a pretty good idea.

We started this whole concept back in 2010. Here in our home market of Utah. The Wasatch Front area of the Wasatch Front is Salt Lake City, Provo, Orem, Ogden is kind of a big, long, skinny, metropolitan area that runs up and down, I 15, it takes you probably an hour and a half, to get from the very bottom of it, to the very top of it, depending on traffic used to not be the case. But now we have traffic, which has been good for values and been good in a variety of ways. But especially those of you from California, and I was in DC this last weekend talking about traffic. Wow.

So we started this in 2010. Back in 2010. If you were buying land, people wanted to have you committed, right, those of you who remember, remember that we were just barely thinking about coming out of the crash. Most markets were not thinking about it yet. But at the time, you could get land for almost nothing. And there’s a lot of cash on the sidelines. And so we figured, hey, we got to we have to try to build or create a product that investors want that can be recession-resistant because that’s what was on everybody’s minds. And I think actually that’s what’s on a lot of people’s minds.

Now they’re wondering, hey, is the shoe gonna drop here? You know, we’re a little traumatized from Oh, wait, and I certainly have my feelings on that. But we’re trying to create a recession-resistant acid here. I would never claim that it’s recession-proof. I don’t think anything is recession-proof. And if you’re that worried about it, maybe buy some bullets in a bunker or something, okay, but we’re talking about recession resistance, something that can allow you to weather the storm.

Until we come out on the other side, we think fourplexes do that really well, for two reasons principally. Number one, when you invest in commercial real estate, nothing wrong with it, right. But you typically have a commercial loan, that’s gonna have a balloon payment in seven or 10 years, sometimes it’s a little more flexible than that. But when you have a balloon payment in seven or 10 years, you’ve got to pay off, you got to refinance, you got to sell that asset that’s attached to the commercial financing. If there’s a recession going on when you’re supposed to pay off that mortgage, that can be a problem. We don’t know what the market looks like, we don’t know what the financing terms are, that are available during a recession like that. So fourplexes are great because you can take advantage of that conventional, true 30-year fixed-rate financing, where you don’t have a VA loan, make your payment every month for 30 years, no one’s coming and telling you you got to pay this thing off. It’s truly recession-resistant, because that you can weather that storm.

Another reason is, you’ve got four tenants and only one mortgage. And I’m not, of course, not just talking about FIG properties here, this would apply to any 4plex, triplex, something like that. But when we have four tenants that are helping us service, our debt, we’re spread out, we’re a little bit more diversified, we get some of those positive effects that come from owning an apartment building where lots of people are paying us, not just one having our fate depends on whether that one is paying us or not. So what something that’s important to understand is the FIG companies.

So FIG itself actually is not a company, it’s a marketing brand. But underneath that umbrella are the four FIG companies and they all have common ownership. And they all have a specific role in this process that gets you what you came looking for, which is a new construction fourplex. So we’ve got the developer, they’re the ones that go find the land, negotiate with the farmer’s fight with the City Council, get the projects approved, go through entitlement, right, that whole development side of things.

We’ve got the builder, right, the builder’s name is Bill Coleman construction, they build in all the states that we operate in, they’re the ones that had this idea of Hey, let’s do four townhomes in a row, and plat it is one tax id that’s going to be that’s probably going to be better than a normal fourplex, which is kind of that boxy, to up to down non managed community type investment.

You’ve also got the brokerage, right, that’s me, we’re the ones that work with you, the investors take you all the way through the process. And you’ve also got the property manager. They’re the ones that do all the lease-up rent collections, tenant qualification, all those kinds of things. It’s designed to be a relatively passive asset. Whenever we have direct ownership of real estate, though, I’d tell you, it’s never going to be completely passive.

For those of you that have purchased turnkey properties, you know that right, you’re gonna have to answer a question, you’re gonna have to make some decisions. Hopefully not much more than that, although it can happen. But we’ve designed this to be as passive as it possibly can be when we deal with a fee, simple direct ownership model of real estate. So a lot of people want to know what the process is like, how is this different from me just going and buying a fourplex on the open market. And there’s a term out there that I think we should pay attention to that’s being used a lot. And it’s called value add, right?

We’ve heard about this in the syndication world, the value add is we go buy a dilapidated apartment complex or some kind of asset that has problems, right, we’re going to acquire it, and then we’re going to do what has to be done. Sometimes it’s legal to work, sometimes it’s just money. Sometimes it’s property management, usually a combination of all of them to get those units making as much money as they possibly can. And therefore the asset is now worth more than your added value. So it’s worth more, and everybody wants that. I’m a real estate agent that deals in multifamily. I get contacted all the time by people.

So you have any value add, right? Well, if you’re what we call an armchair investor, somebody who’s busy, you’re doing other things, you make money, as a physician, you own a company, you’re really busy. You want to get a better deal than average, you’re gonna have to do some kind of value add, you can’t just buy a property with a whole bunch of equity packed into it and not bring something to the table. There has to be a risk that you take on. So let’s compare and contrast for just a second.

What does it look like to buy in a normal fourplex through the standard purchase model that you’re all used to? You call it Bob, the realtor in whatever market is you want to invest in? You’re going to find a property listed on the MLS. You’re going to do a contract, you’re going to close on it. You’re probably going to renovate it and refinance, right? That’s known as the bur strategy by rehab rent refinance. And then you’re going to be in that property, probably at the market cap rate, most likely, okay. And there are some pros to this, there definitely is a time and a place for this strategy you can close now or relatively soon, right?

If you’ve got the money and a willing seller, you can close. And that makes it really 1031 exchange friendly. When we’ve got rigid deadlines, we’re trying to deal with certain amounts that we’re trying to hit to achieve our basis, which makes it very 1031. friendly. And as a result, it’s probably a little bit lower risk, you can really wrap your arms around what kind of asset that is, right? You can inspect it, you can do property management research on the market, and see what you know, what are my rents going to be?

What should they be? Many times you might already have tenants in the property. So a lot of people like that, because it’s a really known quantity. There are some cons that come with it, though, right? Number one is probably going to be really old. That’s not necessarily a bad thing. But a lot of times it can be because it comes with a ton of repairs and a lot of data items with the fourplex. Almost every single investor I talked to agrees with me on this, but and if you’ve already done this, you agree. But if you go hire an agent, say go find me fourplex, you’re going to be pretty underwhelmed by most, if not all of what’s out there.

Right, the cap rates are really compressed, and you really look at it, you go, I can’t believe I got to pay that. To get that. It’s pretty underwhelming. So that’s a con. And then you might have existing tenants in there. We don’t know how well they were qualified. We don’t know how an HOA was set up. If one exists, they rarely do on old fourplexes. And the con, the biggest one of all, for many investors is well, you’re gonna pay market, right? If this thing’s just generating income, people aren’t just gonna give it away.

If you’re giving it away, meaning they’re giving you a really good price, there’s a catch, there’s some hair on that deal, as we like to say around here. And it probably looks something like this. Right? I can make fun of this one. This one’s actually in here in Provo, I lived on that street when I was just a little baby. Those weren’t, they didn’t look that bad when I lived there. They were new.

But you can see what happens over the years, right? roofs get dilapidated. People just leave stuff everywhere. Nobody’s minding the store, right. And if you’re a busy investor, you don’t have a lot of time for drama, you want to make sure that the value of the community is preserved. Right. That’s the idea here. So let’s talk about Oh, sorry, I got scrolling a little crazy there.

Okay, here we go. Catching up. Let’s talk about how purchasing a FIG deal is, is different. And once again, I want to stress the fact that the previous model, right a traditional purchase. That’s great, right, that might be exactly what you need. And we can assist with something like that. But if you’re thinking, hey, I need to take a little bit of time, right, I’m willing to put in some time or some risk or some funds in order to get a little bit above average return. Let’s check it out.

Let’s see how FIG could assist in something like that. So in a big purchase, and I’ll really dial this in for you in just a minute as to how it works, you’re going to select a lot, you’re going to put down a deposit or an earnest money deposit like you would in a normal transaction, then you’re going to close on up and now you go through construction. And that could take 10 to 12 months, and you got to go through lease-up. you’re targeting some forced appreciation there, right?

Anytime that we take a raw chunk of dirt, and we turn it into an income-producing asset. We’re getting some forced appreciation because we gave the market something that it likes. This comes with some cons though. Number one is, unless you have all cash, you’re going to need to get construction financing.

And it’s not free, you’re going to be borrowing somewhere a little bit north of half a million dollars, you have to pay the points on originating that loan and you’ve got construction interest that accrues during that construction process. Right. Another con is you’ve kind of got this window of exposure between when you close on your construction loan. And when it’s done and you go through the lease-up. In theory, things can change. Could rents change or interest rates or, or overall market conditions? You bet they could. So you have to get really comfortable with the submarket the overall economy to go okay, if I’m playing between these two sidelines here if I’m caught, I’m good here.

But if to you if your risk tolerance is this could go outside of it. You know, my stress tests, if you will, and we can help you do that, then maybe this isn’t for you. And then another con is your money is technically on the sidelines. It’s not sitting in an account earning interest for you somewhere else. Although one could argue that that forced appreciation that you get means your money technically isn’t sidelined. I’ve heard all kinds of opinions on that matter. Okay.

So there are some pros to this. Like I said if that forced appreciation if market appreciation is happening in the meantime, that thing might be worth more just because of what the markets doing. I was talking to a builder the other day, we talked about when the market crashed, you know, at so many homes, such an excess supply of homes in some of these markets was there that you could literally buy them for much cheaper than it would have cost you to go buy the materials to build them, right. But the cost of those materials actually didn’t really even go down. It’s only gone up since then. Right. So we do have that going for us. And the fact that sticks and bricks and lumber and concrete and all those things, they just cost more over time, they tend to inflate being the hard asset that they are.

Another pro is you are going to get a brand new fourplex, that’s under builder warranty. So even though it’s new, you can imagine you move some tenants in there, you really don’t know what you have until you’ve been flushing the toilet for a couple of months and really kind of using and living in that fourplex.

So there will inevitably be some repairs and the great thing is most of the time unless they’re tenant negligence, or just deliver damage, those fall under the builder warranty. You shouldn’t have a clogged faucet or, you know, a dripping bathtub, you know, maybe the vinyl wasn’t installed correctly, I don’t know. But those are builder warranty items. And through the integrated property management that we have, you just see that on your statement is maybe a charge for $150, but then it’s zeroed out because of a builder warranty items.

So you’ve got that first year to work the bugs out of the fourplex due to that, you’re gonna get a clean slate on your lease-up, right, you know what the tenant standards are, you know what those people are going to have to adhere to, from the very beginning. I’ll talk about this later, but you get year one bonus depreciation, that one is awesome, it’s gonna save me a lot of money this year. And the bottom line is you get a better cap rate, which equals better cash flow.

Okay, so this is, this is really how an armchair investor can use new construction, to beat the market a little bit, you can go to the other approach, you can pay the market price. Consequently, you can eliminate some of the risks that come with new construction. But if you’re saying I’m willing to push a little bit here, I need a little bit better deal in these markets, you could go new, you can do that with us, you could do it on your own, it’s not as easy as you think.

But you could do that it’s not, it’s not as difficult as you think. So you’re probably going to get something like this, right, a brand new fourplex or the exteriors all maintained where the lawns and flower beds are taken care of the sidewalks are shoveled, the roofs are maintained. Right, you know that in 23 years, that this community holds its value really well because somebody is minding the store.

That’s what we’re after here. So let’s dig into the specifics as to how this would really unfold. And you’re really already kind of taking the first step, which is to visit with fig, you know, you’re here on the webinar to learn more about how this works. Okay, number two is you’ve got to decide on a 4plex, at any given time, we’ve got a couple of projects rolling, that we’re taking reservations and, and some of those might be starting right away, some of them might be a year out, based on when you’re going to have funds, which markets you’d like your timing, your preference, we’re going to talk to you about what some of the best options might be that fit closest to what it is that you’re after.

That’s how we’re going to help you decide on a fourplex and just put those in front of you so that you can decide, then you’re also going to decide on upgrades. Alright, so whenever we call a price for a fourplex, it’s a base price with appliances, you can totally rent it out. Now, we give this option of upgrades because investors have different opinions here and different things that they want to do.

We, of course, do get tons and tons of feedback from our property management team on which upgrades really work meaning when they’re showing these units to prospective tenants. They hear what they’re saying, right? They hear a tenant say, Oh, I hate that floor. Oh, I hate that fridge or Hey, I really like these blinds. Right?

They get that feedback. And they also are the ones that take these maintenance calls and complaints. Right, they know what’s working best and they know which units turnover faster. For example, I have a project in spring, Texas where an investor didn’t put any upgrades into his fourplex. And you can bet he’s always the very last one to rent after buddy picks the other units ahead of his because he skimped on the upgrades.

Based on the project that you’re in, we’ll make some recommendations on Hey, in this one, you probably ought to go with a stainless appliance, you probably ought to go with a better counter, right? Or you could get away with just going kind of a mid-level appliance. It all really depends on the submarket and what the competition is doing and what the tenant demographic looks like. So once you do that and kind of simultaneously will get you pre-qualified for financing.

We have a preferred lender. His name is Lane Aldrich, with First Colony Mortgage. He’s done hundreds of these big construction loans and long term takeouts for us. Nobody’s better than him at it. And you are absolutely welcome to shop. If you’ve got a really good lender, you want to make sure, hey, I don’t want to get taken by this guy, please go, go check it out, make sure that you’re comfortable with it, I think you’ll find that it’s extremely competitive. But most importantly, he’s actually going to get it done.

The way that he does this is he gets a long-term, 30-year fixed-rate approval for you. And he’s going to put that right in a little file, we’re going to come back to it in just a minute. Okay, but this is about the time that you, you decided on a fourplex, you’re doing your upgrades, you’re doing your loan, pre-qualification, this is all within a couple of days of each other.

You’re going to do your purchase agreement, and you’re going to do a deposit. And I say 10 or 10. The reason I say 10 or 10 is if we have not yet recorded the plat. That’s the next step here. Then you’re gonna owe a $10,000 refundable deposit. That’s all that it takes to hold the fourplex. And if you wake up the next day saying, Oh, no, I’ve made a terrible mistake, you get your money back, no questions asked, right? We can’t hold a nonrefundable deposit on a property where the plat has not yet recorded. Now when we get to the next step, that plat recordation.

That’s when we take that 15-acre parcel and we chop it up into 50 different tax ID numbers for this fourplex. That’s when we go to 10% is now do and it’s nonrefundable. So let’s go time. And we’re going to make sure you understand approximately when the plan is going to record when you’re deciding on your fourplex. So you know kind of hate here or when my goalposts are and when certain decisions have to be finalized by or not. Okay, so the plat records we have our 10% deposit in, and usually anywhere from 30 days to a couple of months after that plat recording is when we’re going to start seeing the first construction loans close. Right?

Remember, we’re getting a construction loan where we’re taking this asset from dirt, all the way to income-producing so we can get a better cap rate, some equity, and a better return. That’s what we’re after here.

So now that pre-qualification letter, the 30-year fixed-rate mortgage that Lane Aldrich got you pre-approved for, we’re going to go grab that, we’re going to talk to one of the local banks, we found it’s small regional banks and credit unions that have an appetite for this kind of loans.

If you walk into Chase Bank, and say, Hey, I need a construction loan, for a new construction fourplex in Utah, they’re gonna look at you cross-eyed, they’re gonna have no idea what to do with that, right? That’s like asking the guy at McDonald’s to make your sushi. I don’t recommend it. Okay, so you’re gonna go, we’re gonna take this to one of the local banks, they’re going to review the file, they’ll have a couple of cleanup questions for you about, hey, we need these pay stubs, or can you tell us about this part of your tax return? Okay, just to get that construction loan solidified.

Then you close, when you close on that, that’s when most of the money that you’re going to have into this deal will have come out of your pocket by them. And I’m gonna get very specific on how much that is here in just a minute with kind of a live case study for you. Okay. So now you own a chunk of dirt. In Cypress, Texas, in Payson, Utah, right in Surprise, Arizona, I don’t know, it’s one of those projects that you picked. And you own this chunk of dirt, and you go through the build process, which should take it from 10 to 12 months.

When we get into the home stretch of that construction process, you’re going to hear from us, well, you hear from us the whole way with pictures and drone footage and updates on how your construction is going. If you’re going to be in the area, you really want to go see your fourplex, that’s great, just tell us and we’ll set it up, don’t

Just go wander onto the job site. It’s a job site. That’s complicated legal issues, but it’s your property. And you can see it just coordinate with us and we’ll set it up. So when we get towards the end, you’re going to do your property management agreement with Max property management, that’s figs in house manager so that they can begin the marketing process for your fourplex. And you’re also going to finish out that refinance. Remember, you have a construction loan, right now.

You got to pay that off construction loan is not permanent financing. It’s typically a 12-month term, it’s got to be paid off, and that’s where lane comes back in, pays that off and it’s replaced with a 30-year fixed-rate mortgage. That that is a lot of the reason why to do an asset like this. And then you’re done. Right? It’s mostly that simple.

There are usually a couple of speed bumps here and there some curveballs here and there, for example, lease-up being one of them, which we’ll talk about in just a minute, but I wanted to give you kind of a high-level view of how the process unfolds. This is something that investors find Really, really useful. And I apologize if it looks really busy on your screen. Now, those of you that have really looked into this know that this is a screenshot from one of our proformas.

This is one I picked that’s in Texas. And this is the third page about the top half of the third page. And what’s interesting is, when you’re analyzing not just these deals, but any deal, you got to make sure you’re doing it correctly, and that you’re doing a true apple to apple comparison. Right? I had an investor tell me the other day, well, I can get a six cap all day long in the Bay Area. And I laughed myself silly.

There’s a term going around that it’s kind of started to be referred to as a gross cap rate. That’s, that’s crazy. Okay, you have to actually take into account all your income and expenses. And so if you’re somebody who analyzes that stuff, you’re looking, you’re thinking, there are a few things that look a little odd on our pro forma. But once I explain it, I think you’re going to have the light bulb Go on, if it hasn’t already. So if you look here, I just underlined our purchase price, right? That’s it.

And yours could be a little more a little less than that, depending on upgrades and which one you pick. But this is just an example. Okay. And then I put the market value thereof 795. Right? I always get asked, Well, how did you get that market value? It’s usually a combination of comps and then also us backing into the cap rate that we know that the local market will absorb. All right. So we know that fourplexes or commercial properties were traded at say a 5% cap rate, that’s what we’re gonna back into. So you’ve got a little bit of equity there. All right, on that on that spread. Basically, it means if you turned around and you sold it off, rented, we think that that’s what you’re going to get a down payment, you’re going to put 25% of your purchase price down.

So you see what I just highlighted there. 171 and change. That’s 25% of your purchase price of 686. All right, so yeah, okay downpayment that makes sense, easy. And remember on fourplexes, anything duplex two fourplex is typically a 25% down payment on singles, you can get away with 20. That’s great. I wish we were there with fourplexes. But we’re just not yet.

Here’s a fun one. Buying costs. I frequently get asked Well, what is that $33,000 in buying costs? Well, the first chunk of it is what you’re normally used to whenever you close on any kind of a real estate transaction, right, you’re gonna have your title costs, your appraisal, and some prorated taxes and insurance. And typically, there’s an HOA transfer a few things like that, that’s all very normal.

The big meat of that 33,000, though, is prepaid construction loan interest. If you’re going to borrow half a million bucks, the bank is not going to let you do it for free. In this particular case, the prepaid interest would be about 21,000 of the 33,000. That goes into an account at the bank. And every month when the builder draws against your construction loan, and that balance goes up, the bank is going to charge you the corresponding amount of interest based on what you have borrowed to date. And that’s why construction loans interest only.

It’s a nightmare to track something like that if they tried to do an amortizing nobody wants to do that. So they charge interest only on whatever your construction loan balances for the month, that amount gets debited out of the prepaid interest reserve. That way, they don’t have to hunt you down, you just get a notice every month of what was debited. And I should add to I know because I just signed one myself, I’ve got a couple of these under construction for me right now.

But the builder is going to send you towards the end of every month, a draw statement showing, hey, here’s what we did, here’s how much it cost. And this is all coming out of the construction budget that you will be aware of and be shown a copy of then you sign that and they take that to the bank. The bank says great, they send out an inspector to verify that Yes, you did do underground plumbing. Yes, you did pour the foundation. Yes, you have done a fourth of the framing, for example.

And when the inspector verifies that, then and only then does the bank, release the money to the builder. So the builder never gets paid for work that has not already been done. So that’s the buying costs line item. If you have all cash, you’re going to save a good chunk of that you probably shave I don’t know 25,000 off of there because you save the origination costs of the construction loan as well as the prepaid interest.

If you paid all cash, you could do it that way. And then you could refinance out approximately 70% of your cash once the fourplex is complete. So that’s a good option if it’s available to you and you weren’t going to do anything else with that cash.

Here’s a funny one: Initial improvements. So, I don’t know that title is a little bit misleading to me. Our software only lets us call it that we’ve got some other software in the process of being designed customized to fig. But what we wanted to capture by putting $16,000 in the initial improvements line item was the fact that, hey, if you go through this build process, and we’ve got, say, over a six month period, maybe an eight-month period 240 doors coming on the market.

It’s not like your fourplex is 100% leased up the second it’s done. There’s an absorption period, a stabilization period. Right. So Lane Aldrich, our preferred lender does a cut does one thing to buy some time, right. And I’m about to do this myself, I’ve got to refinance out of a construction loan in spring, Texas. I’ve got lane teeing it up for the first week of December, which means my first mortgage payment will not be due until February one, so buys me a little bit of time.

Also, here in Texas, the development team comps you your first three months of Hoa payments, so that’ll save you a little bit of cash too. So taking those into account. And then also if you just kind of keep 16,000 set aside, you’re gonna get six months or more of Hoa taxes, mortgage insurance.

You’ll get your fixed cost covered for six months, while you go through that lease-up period, it’ll last you that long. And I think in reality is going to last you longer, because we just don’t see people go for six months. Without tenants.

Typically you get 130 to 45 days after completion. 30 to 45. After that, right? It could go faster than that, if it’s summertime, if it’s the dead of winter, it might take you that long, it kind of depends. And so please visit with us about what we expect to happen there. But this just allows you to account for stabilization, and therefore accurately reflect in your projected ROI. What you’re going to do here because like I said, it’s not like it’s at least the first day that it’s done.

The good news is that’s the hardest part. Once your fourplex is leased, and then two years later, a unit or two goes vacant, you know, you’re typically looking at your, I don’t know, 30 day replacement period to get get a new tenant in there. I pulled the data, many of you are curious what the occupancy rate is across figs stabilized project, so I’m not counting stuff that’s going through its first round to lease-up.

We’re counting projects that have been completed and already been through that. And right now our average occupancy is at 95%. So if you add all these up, right, it’s gonna run you about to 2548 out of pocket, by the time this deal is all the way done. Like I said, most of the 171 plus the 33, that’ll be by the time you close on your construction loan, the 16. That’s just an estimate, it’s kind of a placeholder, but know that you’d be able to make it a full six months without receiving a dime in income if you just budgeted that. And like you don’t need that right away to close.

That’s just a suggestion on our part. So if we hop over here to the income column, on the right side of your screen, you see our estimated gross rent, that’s based on comparables in the area, it might be our comparables, it might be surrounding townhomes, apartments homes, we take a blend of that and we project what we think we’re going to get, we put in a 5% vacancy rate out of that, right, because that’s the average across our portfolio right now.

We also add some income for tech package and amenities. So this particular project and actually everything from this one forward is a smart home community. So we’ve got cable and smart home and all the units. So the tenants have this mandatory tech package. This is something that that apartments do, right? If you go buy something at the store, they say in the tax is x and you can’t say, Well, I don’t want to pay it.

I guess you could say it. But if you want to leave with that stuff, you’re paying the tax. Same here, if a tenant wants to rent, they’re paying the tech package at an amenity fee. So by a smart home community, I mean, it’s got a smart lock on the front door, a doorbell cam, a Nest thermostat, and an alarm panel, right. It’s a smart community so they get access to all of that stuff, as well as whatever amenities happened to be in the project in this particular project. I know one of our questions for the q&a was well what amenities are there. This one has a cool little splash pad area, a couple of playgrounds dog park, walking trail. So I would say pretty solid amenities on this project.

So you’re going to get your operating income of 6770. But let’s look at our expenses. Right, We know that this fourplex just sitting there is going to cost money. Right. One of the questions was cleaning its maintenance. And I’m going to talk about that in a second you see that I, I put 75 bucks in there, that’s, of course low, and I’ll explain why insurance looks low too. Okay. We’re going to kind of go down here because I’m going to explain it all as one batch together.

Okay, we see our taxes Association and private money. So the first thing to mention on our association fees, many of these costs that you think should be higher actually shifted into the association, line item. one of their main responsibilities is to carry a master insurance policy. Right? Anytime we have shared walls, or we have a common area community, there has to be mastered insurance because you cannot take the chance that the guy next to you doesn’t have insurance.

And this mattered big time, a couple of weeks ago, in the very first project we ever did in Texas, somebody started a cooking fire and this fire sprinkler system flipped on in that building, right? So of course, it’s the HOA policy that is going to come in and take care of that incident. Right? You can’t risk not having it. The Association also does all of the exterior maintenance on your units, shingles, roof replacement, siding repair, maintains all the common areas. So mowing, lawns, pest removal, snow removal, taking care of the pool, the playground, capital reserves for you know… one day, we’re going to need to repave the parking lot, we’re going to need to replace the pool filter, right? All of that stuff.

You don’t worry about what’s outside of your fourplex you don’t insure the shell of your fourplex. That is what the HOA is there for and that is what they do. And it’s very valuable. I had some clients in town a couple of months ago, showing them one of the projects here in Utah. And one of the tenants there had hung up Pittsburgh Steeler sheets in the window, which I say is offensive on a few levels, but most of all being the value towards the community.

So we told the HOA we totally tattletale and I’m just that’s just a cheap Steelers joke. I don’t hate the Steelers, I’m Steelers fans can be fanatical, I want you to think I’m anti-Steger. Even though I just said you’re fanatical. Anyway, I’ll get on to the on-topic here. So that being said, you can’t get away with parking your car, wherever hanging whatever up in the windows, we want to preserve the value of the community here. And so cleaning and maintenance are low because you are just cleaning and maintaining the inside of a brand new fourplex.

And I totally acknowledge that it is not going to be brand new forever. Eventually, we’re going to have a water heater, we’re going to have something that happens. So ask us for a copy of the pro forma, you’ll see that we have our assumptions program to where our income and expenses, the expenses gradually go up a little bit faster than the income over time to account for the fact that interior maintenance will be a bigger and bigger part of your budget in say 10 years versus right now, the insurance is low there.

Because remember, the HOA covers the master insurance policy, you are going to get what is commonly called a condo policy, or an 806 policy. That’s what ensures from the walls and it gives you some liability protection. Right, a pipe that breaks the inside of the units is something that can be ensured relatively cheaply. Most of our clients tend to get them for about that price in Texas, a little cheaper in Utah and Idaho. Everything’s bigger in Texas, including expenses.

So in order to kind of help offset that, in Texas, our management team charges a 5% management fee, you will probably have a lease-up fee of anywhere from 50 to 100% of a month’s rent, depending on who brings the tenant, your taxes and the private mud fee. I’m not going to get into the reasons for that. But those are going to eventually be added together. Right. And if you’re in Harris County, Texas, and you’re not in this Houston city limits, your water and sewer is handled by a private mud District, which stands for a Municipal Utility District. And one didn’t exist on this property. We had to set it up.

And those typically getting wrapped in as an assessment into your property taxes. But we wanted to break it out in case you checked independently. Hey, what are the taxes here and you see all those are pretty low. They’re not going to be that low. Once that mug gets tacked on there, then it’s going to be what you’re normally used to seeing in in the Harris County metropolitan area. Okay, who All right, let’s go to our next screen. Just to tidy up these numbers a little bit more.

You can see down at the bottom left, which gives us a cap rate of six, seven. And I think you would agree with me I mean, we’re taking into account all of the expenses here. We’re not doing this gross cap rate thing and trying to be pie in the sky. We won’t really want to give you a fair representation, your net, your NOI would be 3820 to positive cash flow of 1059 a month on that fourplex, I want to point out, that’s based on us projecting a 5% interest rate.

So in this particular project, your refi is likely going to be happening next summer or fall on that deal. And so we’re trying to account for some uncertainty and interest rates over time saying that, hey, these could go up. But right now, if you’re refinancing that deal, you’re, you’re anywhere from 4.1 to five to 4.5, depending on credit, prepayments, a few things like that

Your cash flow would actually be a good chunk better. If you’re refinancing this today, I’ll leave it up to you to decide for yourself, if you think interest rates are going to go up between now and then or not, I think with the election and everything that they’re probably going to stay put, maybe even adjust downward a little bit, we’ll have to see.

So you have a really good idea for what our rationale is, behind the numbers that we project, you have an idea for what our process is, like, let’s talk about where we do this. And you already know much of that it’s not really a secret, but we’re looking for a good rent to value ratio.

We’re looking for a good diverse economy with plenty of jobs to where we know that, hey, I’m very likely to be able to find people that want to pay me rent for my property. Right? If you can do that, and you can be patient, then it becomes very hard to lose on an investment like this. We have to do this where we have a local presence. I get asked all the time, hey, you come into Tampa, are you gonna go to Raleigh, you’re gonna go to Indy, right, these are great markets.

We need to have a local presence on the ground where we can hire and expand our builder team, move management staff into place, and really be on the ground operating. This isn’t something that you can do from afar. Some of it, Yes, but you got to have reliable people on the ground. And it’s got to be landlord-friendly, some of you are gonna appreciate this.

If you’re a California and you want to start a business, there are a number of different routes that you could take. You take the five or the eight, just get out of there because it’s not very business-friendly. Consequently, it’s not very landlord-friendly. I have a love-hate with California is kind of my home away from home.

I think a lot of people have a love-hate with it. But we want to be in landlord friendly places like we’ve talked about Starwood farms in Texas. This project is 240 doors total construction is in process. Now if you want to meet us out there, reach out, you can go see this one, you can go see a sister community that’s already built. But there are fourplexes that are ready to go to start construction by the end of the year.

Normally, I don’t have them available that quickly. But a large 1031 exchange buyer fell out of the contract. So we got a couple for you. If you want to get started on construction on a fourplex in Texas that begins by the end of the year. And I told you about the amenities there. We’ve got some good ones. And we’re at that 6.7% projected cap rate. Here’s a little bit of insight as to where this project is.

Cypress is on the northwest side of the Houston metropolitan area, you probably can’t see but I’m waving the mouse here along Highway 290. This is the highway that goes all the way into downtown Houston. You can follow it up to Austin, Texas. So if you’re coming from Austin into Houston, this is the first big city that you see, when you hit the metropolitan area.

What’s great is Cypress has been known for a long time, it’s just kind of a sleepy part of town. There’s not a ton going on there. But it’s really been blowing up lately. Part of that being the expansion of 290 Highway, they’ve widened it to allow for more traffic to flow through the area. Because you can see here, wow, there’s a ton of shopping and schools and everything that you could ever want all within a couple of miles. I poached this map from capital retail properties, their red rectangle over here that says site if you can see that.

They’re actually under construction at the same time that we are, they’re putting up Class A apartments, which we usually like because those are priced well into the $2,000 a month range, it makes ours look a fort affordable. In contrast, they’re putting in a Starbucks there some retail and some medical office and these guys are well well-respected developers and builders and the Houston Metro, we’re happy that they see the same thing that we do.

And right next to us is Starwood Farms, there’s some green space, that’s just a utility easement between us but we’re right next to them. You can see that all the vehicles 24,000 vehicles a day going up and down the road 125,000 a day going up and down the 290. And that’s only going to get bigger because so much more development has been announced to go in through the area here.

So just a couple of highlights. This is a report from Marcus and Millichap. They have good things to say. We want to know if this going to be a place where we can get tenants. Is it landlord-friendly?

They say the Houston Metro has grown substantially over the past cycle adding new households at nearly triple the national pace since 2010. We like that. We like population growth is the market expanded demand increase for healthcare, education, professional services, adding even more job creation? Okay, so we got people, and those people have money even better, okay.

Fewer units, meaning fewer coming online are supporting triple-digit vacancy declines across multiple submarkets, such as in Baytown, and Cypress. Right. So we really love this, the continued fast population growth, Harris County is consistently in the top 10, if not in the top five fastest counties in the country.

For those of you that really like to just dig deep on the data, here are some of our employment sectors showing where you know, where do these people work? What kinds of fields are they in? Houston has kind of a misconception that everybody there is in the oil business. And that’s really not the case, a good chunk of Mar, but it’s no longer dependent exclusively on oil.

We really love what we’re seeing from greatschools.org. For this project, right? ratings of 8 out of 10 on elementary school and 8 of 10, the middle school, and cipher, high school is rated 10 out of 10 on grade schools. org. So if you’re the kind that really believes that, hey, they’re good schools, the tenants will come I’ll be okay. over the long term. You’ve got all green lights here.

So that’s one of the projects coming up. We have another one in Boise, Idaho Metro, specifically Nampa. There are three main cities to the Boise Metro, which is a lot smaller than Houston, right, it’s about a 10th of the size. Well, maybe a little bit bigger than that close to a million people on the Boise Metro. Right, but Nampa, we’ve got 300 doors total. We’re a little out there on construction, it won’t start until this spring and summer in Nampa. Before going through all the horizontal work right now, getting the roads and underground in place.

We’ll see when that construction starts there in May. We have a similar amenities package there with pool clubhouse, playgrounds, dog parks, these kinds of things that the tenants like, they want those things, but many cases, they don’t want to live in a lifestyle community, these really, really expensive apartments that are like the Ritz Carlton, and that might be where you and I live.

But when you’re dealing with working people that have a budget, they want to have some of this stuff, but they can’t afford rents that have a two in front of a meeting $2,000 a month or more per door. The numbers in Laguna farms, I’ll summarize these because I didn’t do these I did it for Starwood farms, we’re at a projected six and a 6.7. cap. Our IRR is very solid there due to the equity and the cash flow that we get decent cash, cash on cash, you can do better maybe on some Midwestern houses or something, but you’ll definitely be giving up some of these other ancillary benefits and your monthly cash flow of a little over 1000 bucks. Once again, I would add that’s assuming your 5% interest rate, which would be one of the biggest and biggest things to influence that. So what do they have to say about Boise?

Right from Boise dev watching the housing market out there? Get this between 95 and 99.5% of all units have people living in them in every single area in Boise, the right fifth-highest increase in overall apartment rents in the country. And the average rent across all these was 983, up from 879. That includes all your just really low-end affordable stuff, too. We get good reports of employment, right.

Amazon just announced this not too long ago on October 10. So just barely over a month ago, that they’re moving forward with a new fulfillment center right there in Nampa, just a couple miles from our project. So lots of new jobs coming into the area. And we see that we’ve got a lot of health care, retail, and those kinds of jobs in the area. And our schools are pretty solid, not quite as good as Cypress but very good for the area where you’re definitely going to get tenants that want to live there.

And a lot of investment-grade properties, I see schools rated, you know, two out of 10 many times if you check them on grade schools org. So those are two that I wanted to dig into with some specifics. But there’s some other stuff out there. For example, we actually had a fourplex fall out of contract and magnet Utah that can start construction within the next 30 to 45 days. So if you really want to get into something in Utah, that’s going to get you up really quick. definitely reach out to me because that could be a good, good fit for you.

We just announced a new project in place in Utah, just go to fig.us and click on the now selling button. That’s kind of a stack flat apartment-style fourplex community right there on the south side of Utah County, which is one of only two ways the growth can go right now, we’re going to be announcing very, very soon a project in Provo, Utah. Also, we’re making our initial foray into the Phoenix metro, we’ve had land under contract there for a while, going through all the initial due diligence, getting everything set up getting our people on the ground. Look for us to announce the first one of those in the next 30 days. We’ve got more second phases coming up in projects in Meridian, Idaho, and Nampa, Idaho.

And if you are somebody that needs existing inventory, then contact us because a lot of times we have clients who may be willing to sell a fourplex they’re going to exchange into more. Or maybe you need something that just now for whatever reason, we can, we can typically drum up existing inventory.

And I already went over the pros and cons of what that looks like. So here’s what I just wanted to wrap up with. Because many times people, people ask me about this, there are multi-dimensional benefits to this to real estate in general that I think they really get enhanced when you do a new construction fourplex or any kind of new construction property for that matter. And I didn’t make this up.

This is a long-held acronym that people talk about right, Real Estate’s ideal because you get income, right, you get depreciation, you guys know this stuff, you get equity, right? Your tenants are always paying down your, your balance, you get that appreciation and get leverage, I wanted to highlight two specific things that kind of take this to a new level. All right, number one, the leverage is unique.

This is absolutely the best use of your 10 conventional loans through Fannie Mae doesn’t matter if you have $2 billion in the bank, Fannie Mae is only going to let you have 1030 year fixed-rate mortgages. That’s it, that’s all you get. So if those loans are allocated to properties that are comprised of 124 doors, why not get 40 doors with your 10 loans?

If your spouse’s working can qualify, why not get 80 doors with your 10 loans, and lock in that true 30-year fixed-rate money, because that is the best inflation hedge that there is, right? If that payment stays flat, and you stay in that investment, your cash flow, your rate of return is only going to get sweeter over time. Now, finally, you don’t have to actually raise your hand, but Raise your hand if you hate taxes.

And I tell you on this one, because please, please, please get accounting advice, right? As far as me talking about this, I’m a guy giving you my opinion on it. But get accounting advice because depreciation on fourplexes is a lot sweeter because number one, you know that when we talk about depreciation, we can depreciate the sticks and the bricks, right? Not the land, but the sticks and the bricks over 27 and a half years. For some reason the IRS has it in their head that you know, your materials are depreciated down to zero after 27 and a half years.

So that being said, there are some limitations on who can take that if you start to make more than $150,000, you actually can’t take that depreciation against your income for the year, it accumulates in a passive losses bucket that you can use later when you sell the property to offset some of your gains. Most of the time, there there are a whole bunch of nuances to that depending on your individual situation. But that’s I’ve said this to multiple CPAs. And they go Yeah, you didn’t completely blast FIMA against the accounting Gods there…

So that’s how it works. Now, you want to save taxes, right? It’s the biggest expense that you’re going to have in your entire life. Any anything we can do to lower what we owe on taxes today is a benefit. It’s more cash, we can save and deploy into cash-flowing assets today, why not lower that. So the first step that we take to do that is to become a real estate professional.

Or maybe your spouse can become a real estate professional. If you spend a certain amount of time in the real estate business, right, you can lift the cap on the depreciation that you can take. And now every year you can have unlimited passive losses. So if you own a bunch of real estate, right, that you can depreciate, you can just really take that and just pile it all against your taxable income and really lower your tax burden.

That’s something that a lot of people do. I see a lot of clients really benefit from us where one spouse is working, they’re getting killed on w two tax. The other one maybe isn’t or is working part-time. They can get away with being a real estate professional and the passive losses they bring to the table can wipe out or in some cases even eliminate the W two taxes that the spouse is incurring at their job. Okay, now, let’s make it better. Right, those of you that have overcome Before, you know that this 27 and a half year depreciation rule doesn’t totally work, when have you ever had carpet last 27 and a half years,

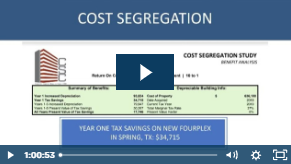

it doesn’t happen. So the IRS knows that there’s certain personal property within your real estate that can and probably should be depreciated faster. And so the way we do this is we hire a cost segregation specialist that we pay to come in and to break down all that personal property. And they can say, Okay, this property, you can depreciate over five years, instead of 27 and a half, this over 10, and this over 15. Okay, cool.

So we took a bunch of this, and we crammed it up into a shorter depreciation schedule. That’s really cool. That saves us a whole bunch of money on our taxes. If we’re a real estate professional or down the road, it can save you more as well. That’s a whole different can of worms. But where does it get even better? Well love him or hate him. Donald Trump in the new tax cuts and JOBS Act gives us bonus depreciation in the first year on new construction.

I tell investors, you should absolutely take advantage of this, if you like Trump, you should thank him because he saved you a bunch of money, if you hate him, you should do it anyway, because you saved a bunch of taxes that he was just going to go build a wall with or something that you disagree with. Okay.

So here is a real-life snapshot, a case study of a client of ours on a fourplex. In spring, Texas, I believe they’re in like a 42% tax bracket. After you take into account federal and state, they were able to cram that depreciation into year one and save $34,715 in taxes, just on the fourplex investment just on one of one fourplex investment, that’s not lowering their taxable income by $34,000.

That’s taking 34,000 off of what they owe. Right? That’s pretty powerful because you still get all of your cash flow and all your other ancillary benefits that come from that ideal acronym that I gave to you. So I’m actually starting one of these myself, I told you, I’m doing a refinance on one at the beginning of December, that I’m going to get on the books and depreciated through case studies to save for myself, I plan on taking that capital and rolling it into other investments and continuing to get ahead because that’s that much less that I had to pay to the taxman. So there’s a chat function with our little setup here.

I’m gonna open it, I think I know how to do that. If you have a question, go ahead and type it into the chat. But if you’d like to talk to us about this, if you’re saying, Okay, I think that sounds pretty good. You know, you’ve shown me how this works for a new construction value adds these markets, I want to learn more about it, then shoot me a message at solson@fig.us. Or you can give me a call, that’s actually my cell phone. So you can call me there. And we can set up a time to chat or, or at least visit for a few minutes. Learn more about us @ www.fig.us.

Question from the audience: Try to explain the cap rate. The way I understood it, the lower the cap rate is, the more valuable property?

Answer: No. The cap rate is is a function that is used to analyze commercial/multifamily real estate. It’s a relationship between the net operating income that you get for it and what you owe on it. Ideally, it’s kind of an inverse relationship. You would like to sell a property at a lower cap rate than what you bought it for. That means you made money. So when we use the term ‘cap rate compression’, it’s just a fancy way of saying that people are paying more and more for these income properties because they perceive them to be more and more valuable.

So we had a question about the depreciation in years one through five. I don’t know if that’s every year if that’s just the bonus first year, I can hook you up with the CPA on that. Because I’m not sure, I’m definitely out of my accounting depth on that question. So I apologize. I just know in that first year that that particular Ambassador was able to save that much money.

I hope to be able to chat with you soon if you feel like a visit with us is going to be beneficial for your investing goals.